If you’re like me every time tax season rolls around you get all your paperwork in order and look through each statement from various banks, brokerage accounts, and entities and everything makes sense -until you start really looking at your forms. All those numbered and sub-numbered lines and titles seem to run together and make taxes so confusing. One group of lines, or sometimes referred to as boxes, on your 1099-DIV Form provided from your taxable brokerage accounts are listed as dividends, but there’s different kinds of dividends. So do you really know what those dividends mean? First let’s look at what a dividend actually is and then we’ll progress to the different types of dividends.

What are Dividends?

Investopedia defines dividends as “ the distribution of some of a company’s earnings to a class of its shareholders, as determined by the company board of directors.” That’s simple enough, right? Not all companies, but some companies reward their shareholders with a small percentage of money as payments, usually quarterly payments, as a thank you for owning stock in their particular company. There are dividend yield strategies in the investment world that speak of how dividends may help one accumulate wealth and be a segment of a semi-reliable income over time. Be warned, dividends can change or be completely eliminated at any time, but strong companies may also increase their dividends on a regular basis as well.

At the top of my taxable brokerage forms are box 1a and 1b. Box 1a is Ordinary Dividends and box 1b is listed as Qualified Dividends. I had to research these two definitions again so I thought I’d share in case you have forgotten or don’t know the difference between ordinary and qualified dividends.

Ordinary dividends are taxed like ordinary or regular income. Whatever tax bracket you fall into your ordinary dividends will be taxed in the same manner as your income. So, for example, if you’re in the 22% tax bracket your ordinary dividends will also be taxed at that same rate.

However, qualified dividends are taxed at your long term capital gains rate. You can find these capital gains tables at various locations around the internet. I referred to the one from Turbo Tax below.

A Reward for Long Term Investors

Qualified Dividends are viewed more favorably by the U.S. tax system and encourages long term investing. Instead of getting taxed at your tax bracket rate the table above shows that you may not have to pay any taxes at all on qualified dividends. If you’re single and make under $40,000 the case would be that you wouldn’t be paying any tax at all on these qualified dividends. In most cases, however, you’ll still have to pay taxes on qualified dividends, but at a smaller rate of tax.

Criteria for Qualified Dividends

There’s one big catch of understanding the difference of these two types of dividends and that is, of course, knowing what makes one dividend an ordinary dividend and the other a qualified dividend.

In order for a dividend to be reported to the IRS and listed that way on your 1099-DIV tax form there are few criteria. One must be “paid by a U.S. company or qualifying foreign company” and “the required holding period must be met.” These two criteria are stated in another of Investopedia’s articles and can be found on various educational financial sites and questions can be asked to your tax preparer or accountant. (See the disclaimer at the bottom of this blog post.)

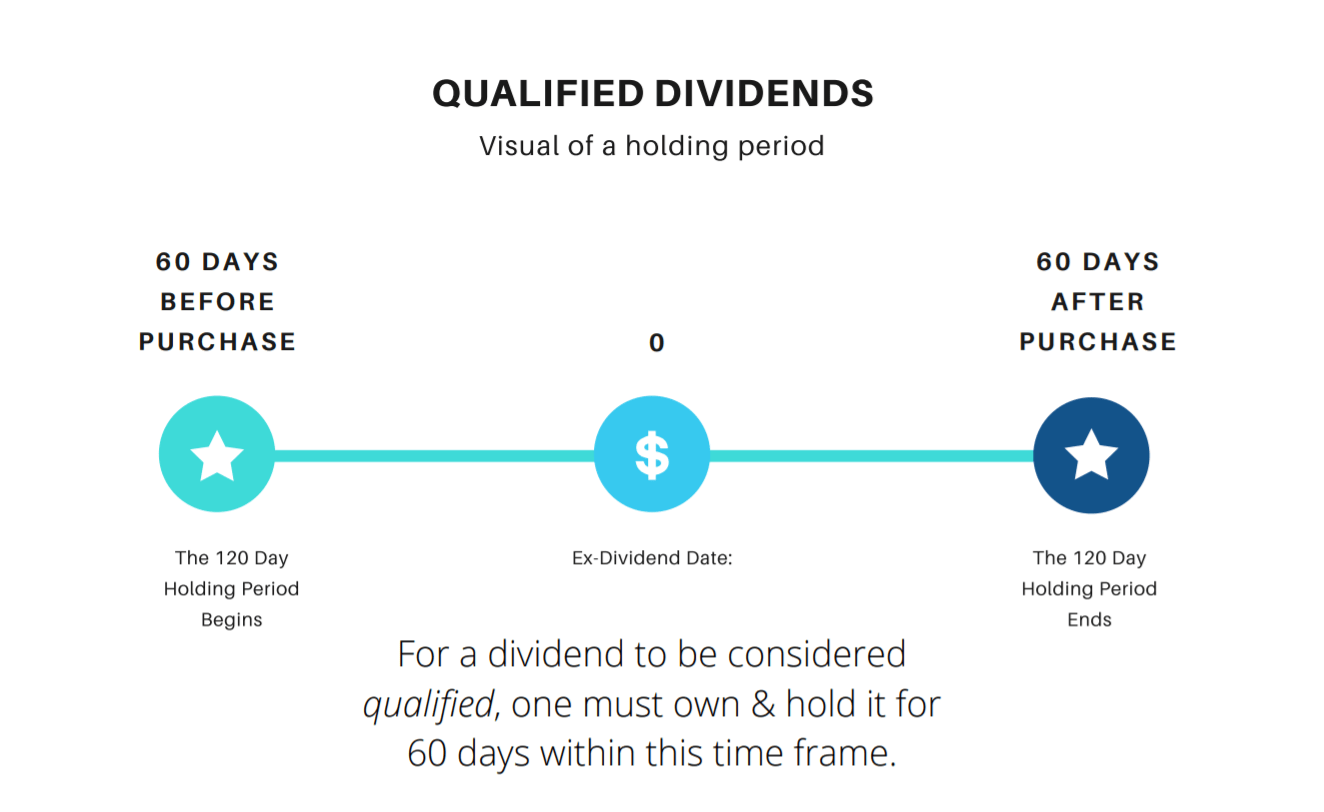

This first stipulation is fairly easy to understand, but the holding period requires a need for a deeper dive. Owning shares of stock with the company a total of 60 days during a specified 121 day time frame makes one eligible for a qualified dividend that is taxed at the cheaper capital gains rate rather than one’s higher normal tax bracket. This specific time period begins 60 days prior to the ex-dividend date. The ex-dividend date counts as one day and the 60 days directly after the ex-dividend date completes the 121 day time frame. The ex-dividend date is significant because this date indicates a person can not receive the dividend if the stock is not owned before this day. See the diagram below.

Understanding the difference of ordinary and qualified dividends helps us become better investors. We can also use this knowledge to help plan our taxes more efficiently.

Until next time

~Quiet Turtle

*Disclaimer: The information provided in this blog and in this website does not and is not intended to constitute financial advice; instead all information, content, and materials presented are for general informational and educational purposes only.

I couldn’t refrain from commenting. Exceptionally well written!

LikeLiked by 1 person

Thank you very much. I’m learning a lot and just want an avenue to share information. Appreciate your kind words.

LikeLike